WASHINGTON, DC — While it was clear the coronavirus (COVID-19) pandemic had a major impact on consumer habits in 2020, the big question that has loomed has been the permanency of that impact.

Cyrille Filott, global strategist of consumer food, and JP Frossard, vice president and consumer foods analyst, of Rabobank, provided insights into that question at the American Bakers Association’s (ABA) NextGenBaker virtual leadership forum, held Sept.14 and 16.

“The longer the virus lingers and we are exposed to these new habits, the more permanent these changes will be,” Mr. Frossard said.

The pandemic’s most significant impacts on the food industry involve how people shop and consume it as well as what items they are choosing to purchase. Changes in workplace norms remain a year later, for example, and show few signs of returning to 2019 norms.

Specifically, many consumers will continue to work from home in some capacity, even as office spaces open. Rabobank estimated that people will work from home at least one more day a week than they did pre-pandemic.

“This is an important trend because it changes consumption,” Mr. Filott explained. “Twenty percent of the location of lunch occasions will change, and the location will shift from business areas to closer to home.”

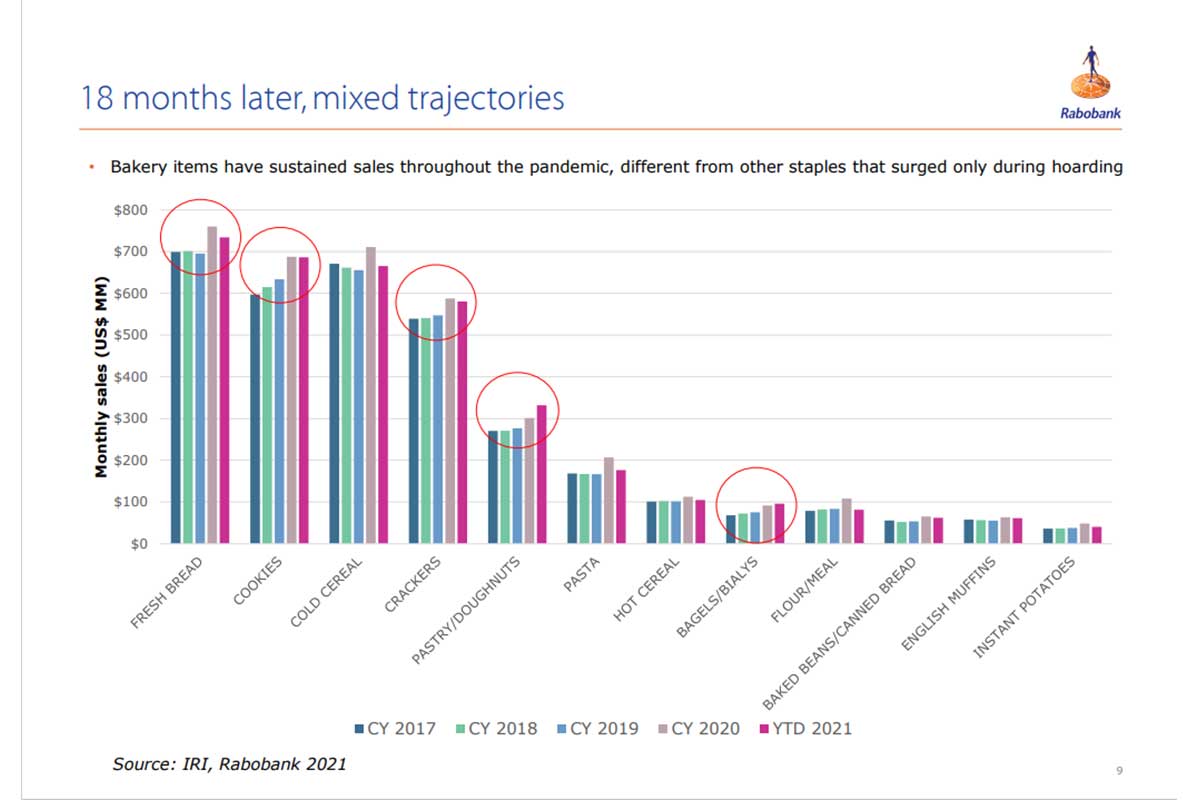

Purchase patterns are also changing. Health and wellness was the biggest trend before the pandemic, and it still has its place. But during the first six months of the pandemic last year, there was a shift toward comfort foods and premium products.

With a renewed interest in cooking, consumers tended to trade up in product quality and splurge on brands. That speaks to a concern during 2020 that did not pan out: the possibility of a long-lasting recession.

“Fortunately, the economic recovery came much earlier than expected,” Mr. Frossard said, pointing to how stimulus checks helped consumers feel secure enough to splurge on food-related purchases. “Since the economic impact was short-lived, the consumer was looking and is still looking for comfort and paying the extra buck for a superior product to replicate that restaurant experience.”

Mr. Frossard said much of the success for donuts and muffins could be because they simplify in-store bakery operations, especially from a labor perspective.

“We’re in the age of low complexity; that’s a hot asset now,” he said.

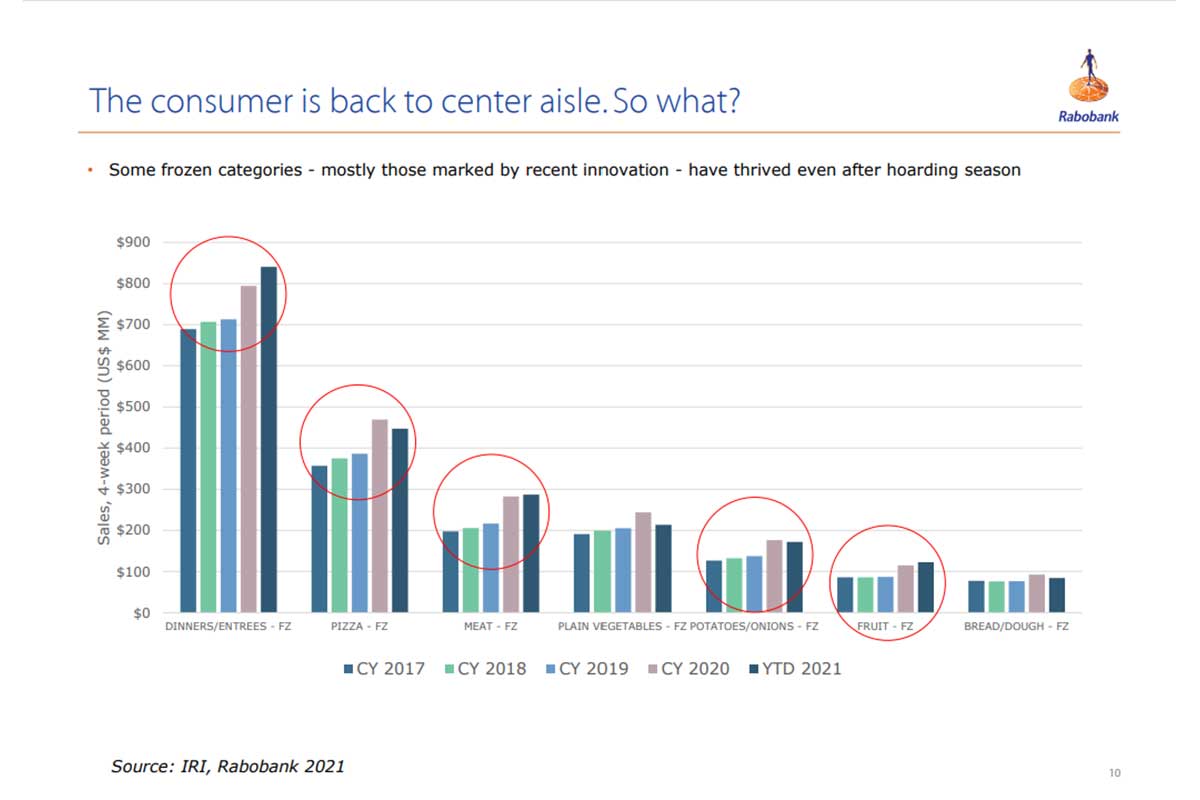

Strong sales for bakery products also point to changing consumer shopping habits. Before the pandemic, most consumers shopped the perimeter of supermarkets, but coronavirus concerns sent shoppers back to the center store and freezer aisles.

Mr. Frossard pointed out that retailers could benefit from reevaluating how baked goods are merchandised in the store to make shopping more inviting and efficient.

He pointed to the ABA’s Power of Bakery report in 2019 showing that only 11% of survey respondent like the way supermarkets are laid out now. While this challenge isn’t new, the pandemic has provided an opportunity to reevaluate and reinvent.

“The momentum is supportive for retailers to revisit this strategy,” he said. “They are trying to save on labor, make things more efficient and trying to get consumers into the store more often because traffic is still down, so it’s up to the industry to push for some change to improve the visibility of the product in the store and make them remember how important bakery is to improving their traffic.”

The biggest shift in consumer shopping behavior involves the explosion of e-commerce. Mr. Filott noted that the jump in online sales seen since 2020 remains above 2019 levels.

“We are seeing the first indications now in second quarter online grocery sales were somewhat down in the US, but they were at a much higher level than in 2019,” he said. “There have been huge investments by retailers into this space.”

While some consumers were using click-and-collect for convenience prior to the pandemic, a greater number of them adopted online shopping for safety reasons and were won over. There are many models of online shopping and the channel continues to evolve to meet consumer needs, whether they are planned purchases or impulse, which had struggled early on.

“We are witnessing a change in how the consumer approaches grocery shopping,” Mr. Filott said. “There might be a consumer behavioral shift that will impact bakery because planned purchases are very different from impulse purchases.”

Different forms of e-commerce can satisfy various types of shopping behaviors.

For instance, direct-to-consumer cuts out any third party between producers and consumers and is well-suited to planned purchases. This model, however, requires a one-to-one relationship with consumers and a strong infrastructure to support the business.

Moreover, marketplace and e-grocers shrink that timeline to 1 to 2 days or even to same day, which has moved the spectrum from planned purchases to more impulse. These models all enjoy higher spending rates from consumers as well as repeat purchases.

Cincinnati-based Kroger recently announced that it is teaming up with Instacart to provide 30-minute delivery, indicating this model will grow and have the support of larger retailers. It remains to be seen, however, if express delivery will completely replace direct-to-consumer, marketplace and e-grocers, Mr. Fillott said.

These various types of e-commerce are important to note because they each provide a different opportunity for bakers.

“All those four channels require different products and how do you, the baker, position for that, and I ask that question so that you can think about, ‘What will be the channels I use in the future, and what channels will I sell into?’ because the consumer behavior is different for each one,” Mr. Fillott said.

Changes from the pandemic are here to stay and have resulted in paradigm shifts in how people eat and shop for food. To keep the momentum of 2020 and 2021 going, bakers will need to continue working with retailers to meet consumers where they are, whether at-home or online.